:

“Clarifying the Provisions of the Sacco Societies (Amendment) Bill, 2025: Addressing Online Misinformation”

Option 2 (Authoritative and corrective):

“A Critical Review of the Sacco Societies (Amendment) Bill, 2025: Correcting Public Misconceptions”

Option 3 (Concise and objective):

“Addressing Circulating Misinformation Regarding the Sacco Societies (Amendment) Bill, 2025”

Recommendation:

Option 1 is the most standard for official communications or formal articles as it strikes a balance between addressing the issue and maintaining a professional tone.")

: Hinga Urges Kenyans to Prioritize Home Ownership Amid Misinformation

Option 2 (Policy-focused): Principal Secretary Hinga Calls for Focus on Home Ownership Initiatives

Option 3 (Concise): Hinga Encourages Kenyans to Focus on Property Ownership Beyond Political Rhetoric

Recommendation: Option 1 is the most balanced and maintains a formal journalistic tone.")

THE SACCO SOCIETIES (AMENDMENT) BILL, 2025: SEPARATING FACT FROM FICTION

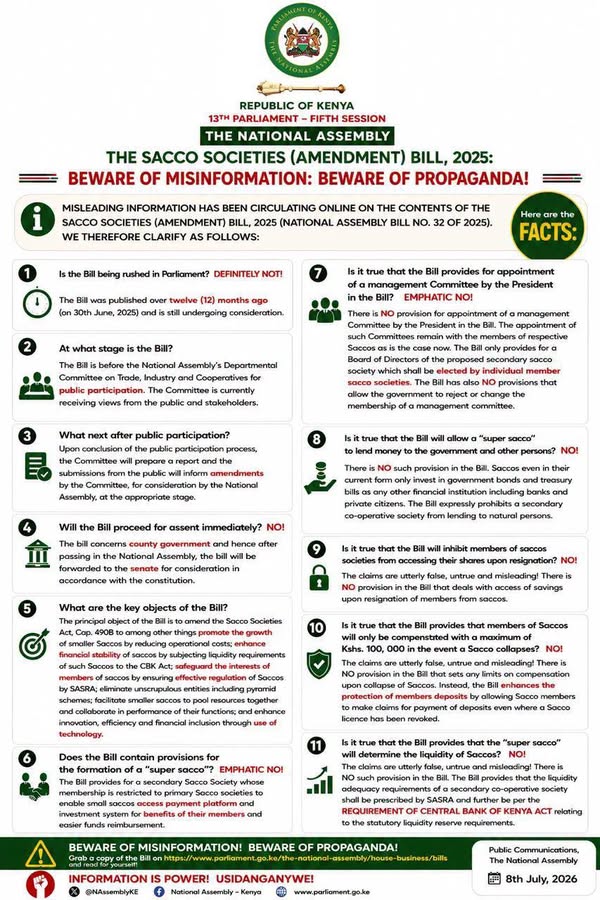

The financial landscape in Kenya has recently been clouded by a wave of alarmist misinformation regarding the Sacco Societies (Amendment) Bill, 2025. Over the past few weeks, various social media platforms—most notably Facebook and WhatsApp—have become conduits for speculative claims suggesting that the government intends to seize Sacco deposits, impose punitive new taxes on member savings, or force mergers between independent credit unions. These narratives, often presented with inflammatory language, have triggered unnecessary anxiety among millions of Kenyans who rely on the cooperative movement for their savings and credit needs. It is imperative, therefore, to scrutinize the actual intent of the proposed legislation and clear the fog of propaganda that threatens to destabilize the sector.

At its core, the Sacco Societies (Amendment) Bill, 2025, is a legislative response to the evolving complexities of the digital financial age and the need for enhanced consumer protection. The primary goal of the amendments is to strengthen the regulatory oversight mandated by the Sacco Societies Regulatory Authority (SASRA). Far from seeking to undermine member autonomy, the bill aims to shield depositors from the risks associated with liquidity crises, poor governance, and the integration of unregulated digital loan applications into the Sacco ecosystem. By aligning the legislative framework with international best practices of cooperative governance, the government intends to professionalize the sector, ensuring that Saccos are better equipped to handle modern financial shocks without endangering the hard-earned deposits of their members.

One of the most persistent, yet demonstrably false, claims circulating online is that the government intends to “tax the savings” of Sacco members. Financial experts and legal analysts have clarified that the Bill contains no provisions for the taxation of individual members’ monthly contributions. Instead, the focus remains on ensuring that Saccos maintain adequate capital buffers to mitigate the risk of insolvency. The propaganda machine has deliberately conflated “capital adequacy requirements” with “taxation,” a misdirection designed to incite public outrage. In reality, these measures are designed to ensure that when a member reaches a point of retirement or experiences a financial emergency, the Sacco—not the government—has the liquidity to fulfill its obligations.

Furthermore, the discourse surrounding the bill has been marred by hyperbolic claims regarding the erosion of Sacco independence. Critics suggest that the amendments will grant the regulator excessive powers to intervene in the daily affairs of cooperatives. However, a deeper reading of the Bill suggests that the regulator’s enhanced powers are strictly tethered to the protection of member funds, particularly in instances where a Sacco’s board of directors is found to be engaged in gross financial misconduct or fraudulent activities. In this context, the Bill acts as a final safeguard, preventing the total collapse of Saccos that have historically fallen victim to mismanagement, thereby protecting the interests of the rank-and-file members who traditionally have little recourse when a board fails.

It is also crucial to address the disinformation regarding the digitisation mandates suggested in the Bill. Alarmists have falsely claimed that these mandates are an attempt to integrate Sacco databases with state surveillance systems. In truth, the proposed amendments seek to enforce cybersecurity standards to prevent the rampant fraud currently plaguing the sector. With the rise of cybercrime, many Saccos have been vulnerable to data breaches that expose members to unauthorized withdrawals and identity theft. By standardizing the IT infrastructure and cybersecurity protocols, the Bill merely aims to create a secure digital environment where members can conduct transactions without the looming fear of being hacked, professionalizing the digital experience for the common depositor.

Ultimately, the Sacco Societies (Amendment) Bill, 2025, is a necessary evolution for a sector that holds a significant portion of the country’s national savings. While public scrutiny of any legislation is a healthy democratic process, it must be rooted in fact rather than manufactured fear. The cooperative movement in Kenya thrives on trust, and misinformation that targets that trust ultimately harms the members more than the institutions themselves. As the bill undergoes public participation and parliamentary debate, it is essential for stakeholders to engage with the actual text of the legislation and ignore the malicious narratives propagated by those seeking to cause panic for political or personal gain. Stability, not state control, remains the ultimate objective of these long-overdue reforms.

: Hinga Urges Kenyans to Prioritize Home Ownership Amid Misinformation

Option 2 (Policy-focused): Principal Secretary Hinga Calls for Focus on Home Ownership Initiatives

Option 3 (Concise): Hinga Encourages Kenyans to Focus on Property Ownership Beyond Political Rhetoric

Recommendation: Option 1 is the most balanced and maintains a formal journalistic tone.")